The industrial real estate market is settling into a new normal after a frenetic few years, with construction of new facilities tapering off yet rents continuing to rise.

Bill Waxman, vice chair, Cushman and Wakefield, and Eric M. Bernstein of Eric M. Bernstein and Associates, LLC, served as panelists for the annual regional industrial real estate update during the NJTPA's

Freight Initiatives Committee (FIC) meeting on Feb. 20.

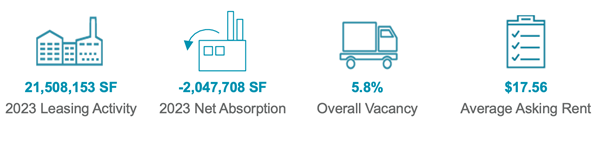

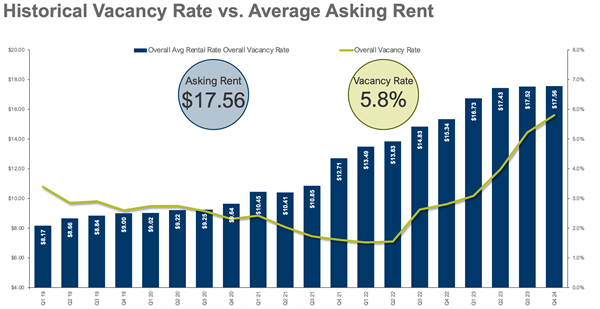

The boom in warehouse construction had been driven by the need for companies to meet strong consumer demand for goods, particularly in the pandemic when consumers turned to online shopping in a big way. That construction is beginning to taper off, according to Waxman. He expects new construction starts will continue to decline this year. The 5.8 percent vacancy rate is still well below the 10-year average of 8 percent.

The market recorded “negative absorption” – supply of building space outstripping demand for it – due to a record 14.4 million square feet of new buildings delivered that all became available at once. The shift began at the start of 2023 after a decade of positive absorption, Waxman said.

Yet rents continue to grow even though vacancy also grows - “It defies logic,” Waxman said. That’s because many renters are downsizing from non-Class A buildings -- older industrial facilities located in poor markets and elsewhere -- in favor of smaller spaces in more modern Class A buildings which are commanding higher rents. Many of the newer buildings are in the south and western areas of the region.

“They may be vacating 200,000 square feet of several older buildings and moving into one, more efficient building further south or where buildings are less expensive, so they’re absorbing 150,000 of new Class A building but leaving 200,000 square feet of older, industrial product on the market,” he said. “That’s why 100 percent of that negative absorption was in B and C buildings and positive absorption was all within Class A.

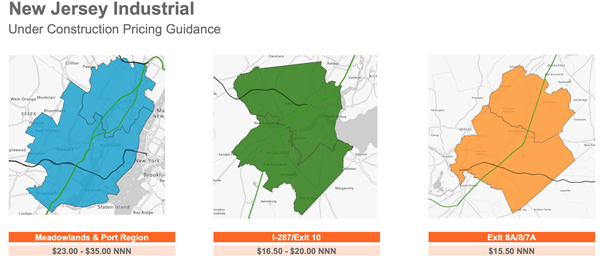

Companies traditionally in Linden, Elizabeth, and Edison are saying, “I don’t need to be there,” and decamping for cheaper rents in areas like Hamilton, Somerset, and Parsippany, according to Waxman. “That’s one of the reasons why you’ll see Class A continue to be strong,” he said, with more efficient buildings and a flight to quality continuing.

The ability to build new buildings in New Jersey, however, is becoming much more difficult. “A lot of towns are saying we have enough, we don’t want more warehouses," Waxman said. “Demand is falling so builders are waiting and not going to spec a building."

Bernstein thinks the slowdown in buildings is a good thing. Before COVID, he said most developers wanted nothing to do with warehouses.

“In the old days, when you built a strip mall, you had some idea what kind of clientele you were seeking,” Bernstein said. Now, when an applicant is asked what sort of warehouse they will build, they won’t commit, despite 13 categories to choose from. The answer typically is: “It won’t be a fulfillment center.” This lack of detail leaves town officials in the dark about potential impacts and has led to increasing resistance to the facilities.

If developers adequately planned ahead they could explain the pros and cons of the category of facility that they were seeking. But that is not occurring.

“You can’t get what seemingly is a reasonable answer," Bernstein said.

The

presentations and a

complete recording of the FIC meeting are

available here.